Create an Account

Create an Account

Login/myAPPA

Login/myAPPA

Bookstore

Bookstore

Search

Search  Translate

Translate

Value management is a concept that embraces facilities design while balancing appropriate but sometimes competing program, quality, performance, and cost requirements, while considering the total cost of ownership (TCO) throughout the design process.

Although many needs compete for inclusion in all capital projects, a long-term view of capital assets represents a continuing investment in education facilities.

Integrated Value Analysis

The design process and facilities continue to increase in complexity, with an ever-increasing awareness of the built environment, natural resource conservation, and sustainability. Continual product development and data storage and retrieval give the designer alternatives.

Competing needs overlap with disciplines on the expanding design team and require more coordination and evaluation. Owner requirements and the architectural discipline have the largest cost impact; early decision making has a substantial cost effect; each discipline overlaps the other; and large savings usually occur earlier in the process and in overlapping areas.

Management is integral to the design process. The 90/10 rule indicates that decisions in the first 10 percent of the project determine 90 percent of the outcome (e.g., schedule and cost). Life-cycle cost and value management are invaluable tools for cost-effective decisions during the entire design process. A statement of maintenance impact is needed because new materials and systems in building designs produce new maintenance problems for the facilities group.

Designers face an array of complex decisions in designing a building, and TCO (i.e., dollar per square foot value of facility; all facilities-specific costs divided by estimated building life span, then divided by total gross area) is often neglected. In designing facilities for maintainability, the owner prepares a maintenance profile, with staffing, energy, building systems upkeep, and replacement budgets. Over building life, original capital costs and maintenance and operational costs are almost equal, but after adding recapitalization costs to

TCO, the final cost of owning and operating a facility often exceeds initial cost. Systems should be designed to respect the class of operating personnel and owner philosophy. If funds are difficult to obtain for replacement and regular maintenance, materials and systems must be selected with a focus on long life and minimum regular care to balance initial costs and continuing maintenance costs.

Value Management Reviews

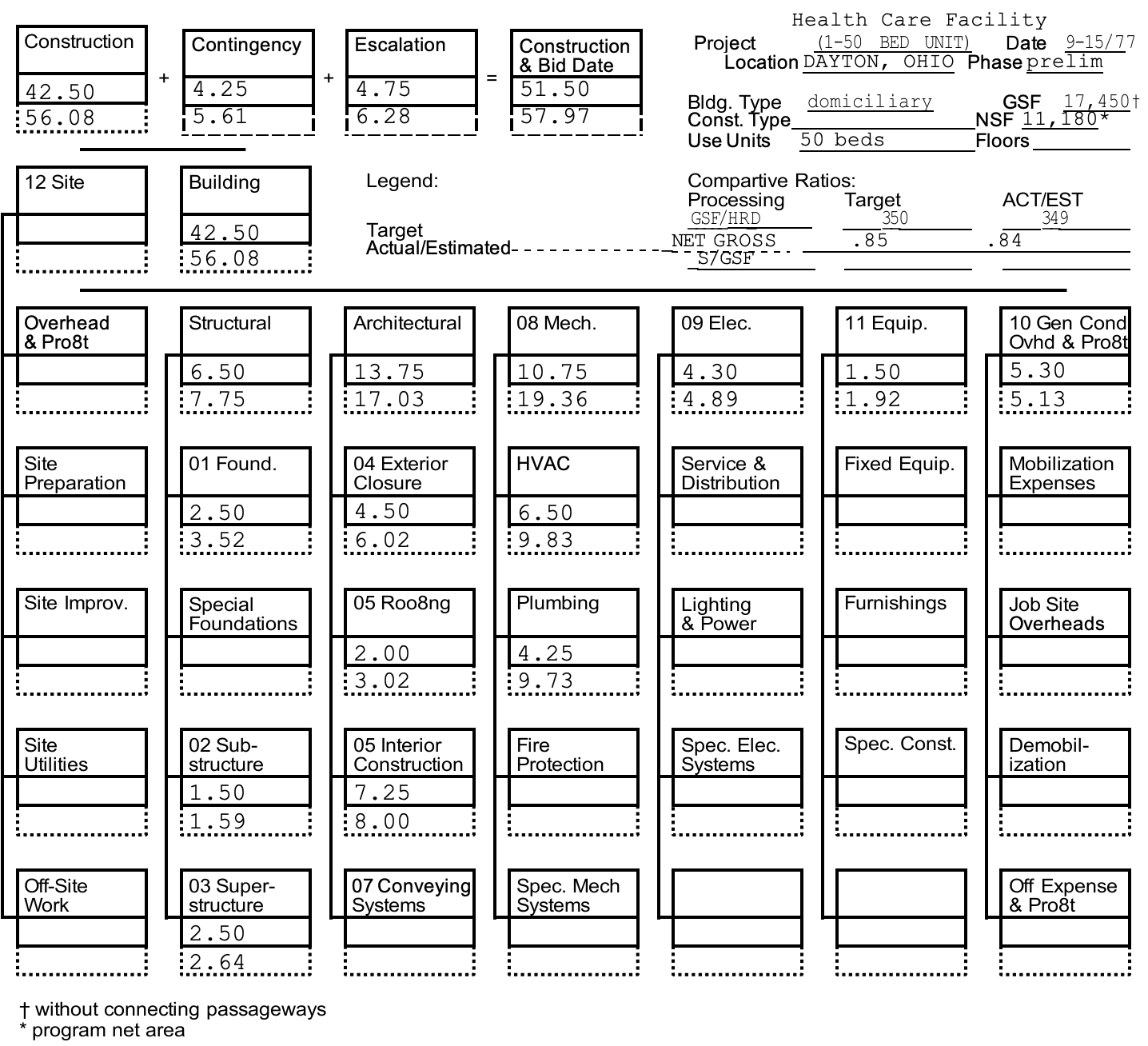

Value management is rooted in a more traditional approach to project budgeting and review, value engineering (to date more of a cost-cutting tool than a decision-making tool, which is its intended purpose). A project team (and independent specialty consultants), led by a certified value specialist, performs value management, using a job plan (e.g., information gathering, functional analysis, creativity, development, presentation). The value management process uses value engineering principles (most effective in early design stages, per the 90/10 rule) to involve appropriate people in the evaluation and decision-making process. Value engineering tools produce optimal results (e.g., layout, structural bay sizing, floor-to-floor height, exterior closure, finishes, mechanical and electrical systems, lighting, furnishings, net-to-gross floor areas, energy conservation, systems integration, roofing systems, constructability) and support decisions on whether to renovate, expand, replace, substitute, or eliminate facilities. Project cost data are organized in a cost model using the UniFormat system, showing architectural and mechanical areas that offer the best savings potential and deserve in-depth study. Analytical value engineering phase evaluation of alternatives uses a weighted evaluation form to compare each criterion to the others to determine relative preference. Using value engineering, design professionals identify required functions, develop alternatives, and select the most cost-effective long-term solution, so owners receive the optimal return on investment. Value engineering produces savings that exceed the cost of the process; savings ratios of 2:1 are routine, and 20:1 is not uncommon. As a rule of thumb, value engineering finds savings of 5 to l0 percent of total project costs, with typical value engineering costs at 0.2 to 0.5 percent of construction costs. A key to developing meaningful solutions is using an experienced multi disciplinary team not involved in the original decisions, led by a certified value specialist with extensive experience. Whether the institution uses an on-staff value engineering officer or a consulting firm, the facilities staff, project manager, design team, users, and affected stakeholders must be involved in the process (see Figure 4.10).

Figure 4.10. Cost Model

Life-Cycle Cost Review

As value engineering identifies alternatives for better value, the analysis method includes economic assessment and all significant ownership costs (e.g., initial costs, financing, energy, maintenance, taxes, alterations and replacements, salvage value) over an economic life, expressed in equivalent dollars. To reduce time and complexity in using life-cycle costs, the elements that are the same in any of the options are identified and removed or fixed, with significant costs for each alternative isolated and grouped by year or time spans and all costs converted to current dollars.

Although the 90/10 rule applies, it is equally important to focus on the appropriate decision-making level to ensure that the greatest impact is realized. The major impact of life-cycle costs occurs in concept, schematics, and design development. Life-cycle cost can be used during the predesign phase to assess project feasibility (e.g.,

$1 saved from operating costs via better planning or design equals $10 to $12 in construction cost reductions). Comparative costs (e.g., high initial costs, continuing costs) are associated with each building system. Life-cycle costs are evaluated in tabular form, including initial costs, replacement and salvage costs, and annual costs in present value to comparatively analyze alternatives versus original system design.

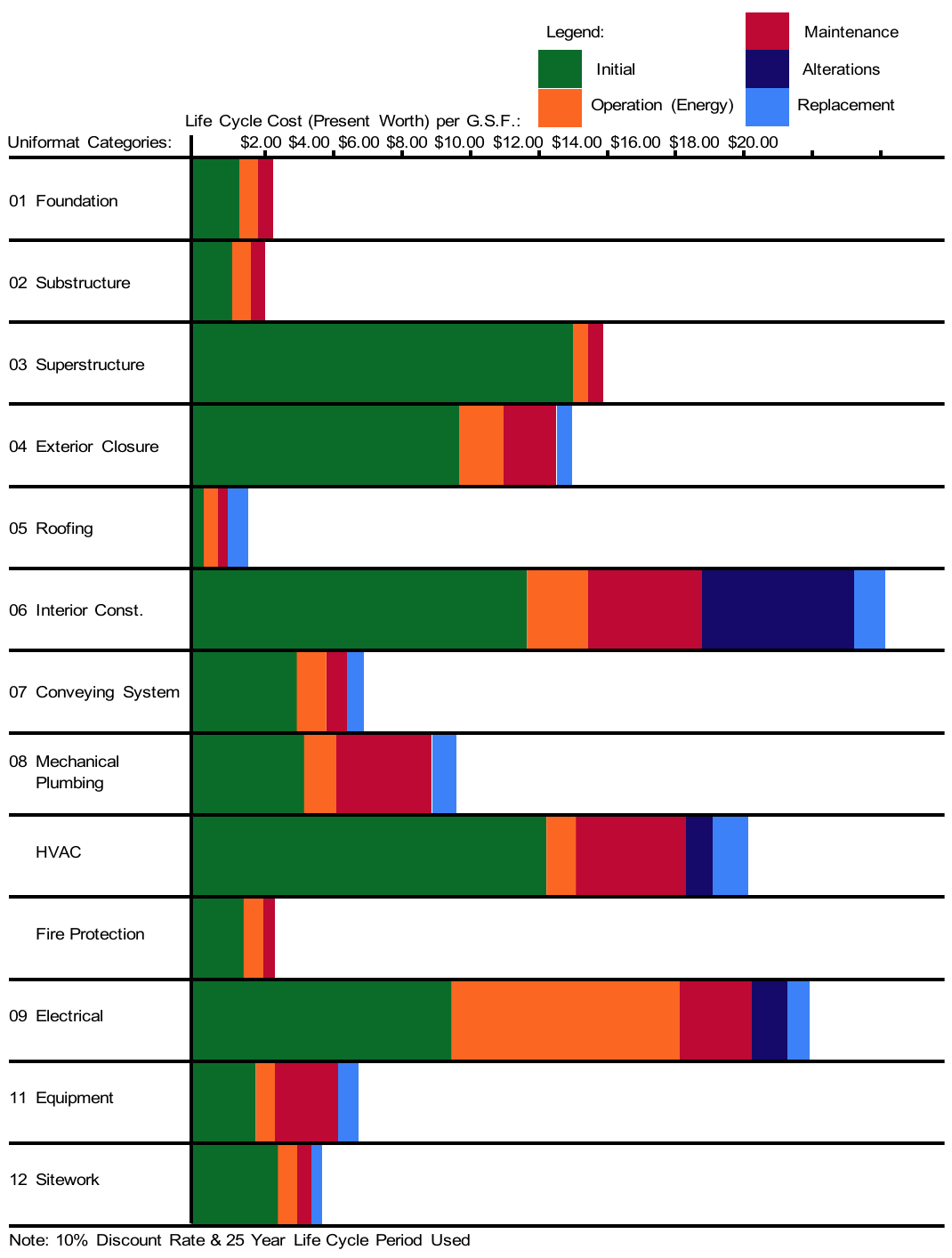

Current and future costs are brought to a common point in time using two methods, conversion to current cost (present worth or net present value [NPR]) or to annual payments (annualized). In value decisions, a common mistake is using incremental marginal NPR results to determine whether to make a marginal investment in the next level of a mutually exclusive alternative; NPR is calculated against the original choice, not other mutually exclusive choices (see Figure 4.11).

Figure 4.11. Life-Cycle Cost Distribution, Present Worth, for a Typical Office Building Contractor Review

Source: Dell’Isola, Alphonse J., and Stephen J. Kirk. Life Cycle Costing for Design Professionals. New York: McGraw-Hill, 1981.

The constructability of a particular design has a profound impact on cost and time needed to build the facility, so evaluation of proposed building systems can be valuable during design, but contractor experience and expertise determine actual review value. The review occurs early in the design to provide the greatest benefit, and making it part of the value management process yields the greatest results; if it is part of the value engineering study, project issues related to ease of construction are evaluated. Some common project delivery approaches (e.g., construction management, integrated product delivery) encourage this type of early contractor involvement. For some government projects, value engineering change proposals give the public works contractor the chance to offer better-value alternatives.

Maintenance Impact Statement

A maintenance impact statement offers maintenance recommendations for equipment and annual operating costs, with costs converted to present-value dollars for life-cycle evaluation. Evaluation criteria include staffing and material costs for system and building operation and maintenance, replacement costs and life of equipment and building systems, and annual energy consumption. Maintenance information can be compiled in a format for use with value engineering and life-cycle cost forms with seven categories (structural, architectural, mechanical, electrical, equipment, site, and other). Data are provided for annual maintenance cost (labor, material equipment), energy demand, replacement life in years, and percentage replaced. These forms identify unit of measure of maintenance and describe the maintenance performed, but historical data could be substituted for inclusion in life-cycle cost evaluations as part of the value engineering project study.

Leave a Reply

You must be logged in to post a comment.